The fundamentals of eCommerce are simple - purchase or create a product and sell it online. It’s the nagging administrative hassles that aren’t quite so easy to handle. And of those, the administrative detail that gives online sellers the most trouble is sales tax.

This article will provide online sellers with an overview of everything you need to know about sales tax nexus, how to calculate sales tax in different states, and more.

Let’s dig in.

What is Sales Tax?

Sales tax is a tax on a transaction, as its name suggests. It’s paid by consumers but collected by retailers, who hold it in trust until remitting it to the appropriate tax authority along with a sales tax return.

There’s no federal or national sales tax in the United States. Instead:

- 45 states and Washington, D.C. have a state sales tax.

- 37 states allow local sales taxes (including Alaska, which has no state sales tax).

- 6 states allow home rule (Alabama, Alaska, Arizona, Colorado, Idaho, and Louisiana), meaning cities, counties, or special tax jurisdictions can collect and administer sales tax independently.

- 5 states have no state sales tax (Alaska, Delaware, Montana, New Hampshire, and Oregon, or the NOMAD states).

All told, there are more than 13,000 sales and use tax jurisdictions in the U.S., each with its own rate, boundaries, and reporting code.

Sales Tax Jurisdictions

These numbers help explain why sales tax compliance is so complicated; sales tax rates, product taxability rules, and regulations differ from state to state, and sometimes even from city to city. Companies with an obligation to collect sales tax in multiple states need to understand and comply with all pertinent sales tax laws.

The first step toward compliance is figuring out where you need to collect sales tax.

Who Needs to Collect Sales Tax?

Whether you need to collect sales tax in a state (or locality) depends on nexus, which is simply a link or connection between a taxing jurisdiction and a business.

In other words, a state cannot require a business to register then collect and remit sales tax unless the business has nexus with the state. But businesses with nexus must register and comply with applicable sales tax laws.

How is Nexus Established?

Until relatively recently, nexus was based exclusively on physical presence. A state could require a business with a physical presence in the state to collect and remit sales tax, but it couldn’t do the same for a business with no physical tie to the state. Most states provide a sales tax calculator so you can see exactly how much you need to collect.

Physical Presence

Physical presence seems straightforward, but it can be surprisingly nuanced. A brick-and-mortar store or office constitutes physical presence, of course, but does a traveling sales representative or employee? What about systematic solicitation via catalogs or online ads? Inventory in the state?

Every state has a different answer to each question — some more well defined than others. For example, physical presence nexus is established if an employee or representative conducts business for:

- One day in Colorado or Texas

- More than two days per year in Arizona

- At least four days during a 12-month period in Minnesota

If you send employees or representatives into another state for any reason, you may create nexus. Storing inventory in another state can do the same. When in doubt, contact a trusted tax advisor.

Stretching Physical Presence: Affiliate and Click-Through Nexus

States were interested in taxing out-of-state sales long before Jeff Bezos sold his first book on Amazon.com. Once businesses could use the internet to market and sell to consumers in all states, many states redoubled their efforts to tax remote sales. To that end, they broadened the definition of physical presence to include:

- Affiliations with in-state businesses (affiliate nexus)

- Links on websites operated by residents or businesses in the state (click-through nexus)

Today, out-of-state businesses can establish nexus in many states through in-state affiliates, internet links, inventory, remote employees, trade show attendance, traveling representatives, or other ties.

And thanks to the United States Supreme Court’s decision in South Dakota v. Wayfair, Inc., it’s also possible to create nexus through economic activity alone (economic nexus) — no physical presence necessary.

Beyond Physical Presence: Economic Nexus

In South Dakota v. Wayfair, Inc. (June 21, 2018), the Supreme Court of the United States overruled the longstanding physical presence rule. Having a physical presence in a state still creates nexus; Wayfair simply gives states the option of taxing businesses with no physical presence in the state.

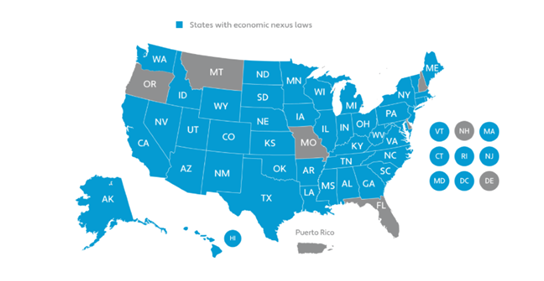

Today, just two years after the decision, all but two of the 45 states with a statewide sales tax have adopted economic nexus law. A growing number of cities and counties in Alaska have done the same, and there are efforts to enact economic nexus in the holdout states of Florida and Missouri.

What is Economic Nexus?

Though no two economic nexus laws are exactly alike, all base a sales tax collection obligation solely on a remote seller’s sales activity in the state.

How much sales activity does it take to trigger economic nexus? It depends on the state.

States with economic nexus laws as of June 15, 2020

Exception for Smaller Sellers

All states except one provide an exception for small remote businesses, meaning an out-of-state business must have a certain volume of sales in the state (the economic nexus threshold) to trigger economic nexus.

Kansas is the outlier. According to the Kansas Department of Revenue, “Kansas can, and does, require on-line and other remote sellers with no physical presence in Kansas to collect and remit the applicable sales or use tax on sales delivered into Kansas.” In other words, just one sale into Kansas could create nexus for an out-of-state seller.

Economic nexus thresholds in all other states are based either on sales volume or number of transactions, or sales volume and number of transactions. For example:

- Alabama: Sales only ($250,000)

- California: Sales only ($500,000)

- Illinois: Sales ($100,000) or transactions (200)

- New York: Sales ($500,000) and transactions (100)

And it’s not just about math, because you need to know which sales are included in each state’s threshold. Some states include only taxable sales of tangible personal property, some taxable property and taxable services, some taxable and exempt property and services, and so on. Some states include wholesale sales in the threshold, and some don’t. Some include intangible personal property (e.g., digital goods and services) and some don’t. This seller’s guide to nexus rules and sales tax collection requirements provides details about all sales tax nexus laws.

Before ever dealing with the hassle of collecting, filing, and reporting sales tax or validating exempt transactions, you need to figure out where you have a sales tax obligation. This free sales tax nexus risk assessment can help.

How to Register for Sales Tax

Once you determine you have a sales tax collection obligation in a new state, you need to register with the state tax authority (and any necessary local tax offices). Some states give businesses a little leeway, requiring registration within 30, 60, or 90 days of crossing an economic nexus threshold. In other states, out-of-state retailers must register to collect and remit sales as soon as the economic nexus threshold is crossed (i.e., before the next invoice).

Registering is typically a straightforward process. You’ll need to provide the tax department with a certain amount of information, including the legal name and address of the business, identifying documents for the owner (i.e., driver license and/or social security), federal and/or state employer identification numbers (FEIN or SEIN), and projected monthly sales in the state.

There’s a fee to register for a sales tax permit in many states, including Arkansas and Connecticut. But sales tax permits are free in California, Florida, and several other states. Most everything about sales tax is subject to change, so check with the state tax department for the most up-to-date information.

Registering in Multiple States

Businesses required to register in multiple states should consider registering through the Streamlined Sales Tax Registration System (SSTRS). The program greatly simplifies sales tax registration in one or all of the 23 Streamlined Sales Tax (SST) member states that have taken steps to reduce the costs and burdens of sales and use tax compliance for out-of-state sellers.

If you qualify as a volunteer seller in an SST state and opt to use an SST Certified Service Provider (CSP) to calculate and remit sales tax and file returns, the state will compensate the CSP for its software and services. In other words, volunteer sellers are eligible for free sales tax calculation and reporting services in SST member states.

How to Determine Taxability

Once registered in a state, you need to determine which of your sales are taxable and which are exempt and calculate sales tax on taxable transactions. While most transactions are subject to tax in Hawaii, New Mexico, and South Dakota, most other states provide a number of sales tax exemptions.

For example, information services and personal property maintenance are subject to sales tax in Texas, but personal services like haircuts are not. Florida taxes amusement and recreation services but not services performed on tangible personal property (e.g., repair services). North Carolina generally taxes installation, maintenance, and repair services, but many other services are exempt. And so on.

Tangible personal property is typically taxable, but there are many exceptions to that rule. Fur coats and sports equipment are taxable in Minnesota, but jeans and t-shirts are exempt. Digital products like eBooks and streamed music are subject to sales tax in Pennsylvania but exempt in California. The taxability of candy is all over the map:

- Subject to the general rate of sales tax in Idaho and Mississippi

- Subject to a reduced rate in Missouri and Virginia

- Fully exempt in California and Washington

State departments of revenue are a terrific source of information, but it can still be challenging to determine which products and services are subject to sales tax in a state. The fact that taxability is subject to change doesn’t help.

If what you sell is taxable, how do you calculate sales tax?

How To Calculate Sales Tax

Sales tax rates vary by location (remember the 13,000+ sales tax jurisdictions mentioned up above?).

Most states base sales tax rates on the place where the consumer takes possession of the product or service (destination sourcing), though some base sales tax on the location of the seller (origin sourcing), and some use a combination of both sourcing rules. Adding to the complexity, some states require sellers to collect tax on shipping and handling charges, while others don’t.

You can use a sales tax rate calculator to find the sales tax rate for an address, but that’s not a viable long-term solution for businesses required to collect sales tax in multiple jurisdictions. Sales tax rate calculators also don’t account for the variations in product taxability discussed above.

Online shopping carts like 3dcart typically have sales tax engines that facilitate sales tax collection. If properly set up, they’ll charge the proper rate of tax for each taxable sale. The kicker is that they need to be updated when product taxability rules or rates change.

While it’s possible to calculate sales tax manually, you’ll need to dedicate a substantial amount of time and research into getting it right. Otherwise, you may want to hire a tax professional to handle your obligations.

However, there’s a more automated solution. Sales tax software makes managing sales tax much more manageable. For example, Avalara AvaTax connects with more than 700 prebuilt integrations in accounting, ERP, ecommerce, shopping cart, and other applications, enabling sellers to streamline sales tax collection and compliance.

Sales tax software can also help you manage the exemption certificates needed to validate exempt transactions (e.g., sales for resale). These must be kept up to date and on file; in the event of an audit, the auditor will want to see them.

Finally, sales tax software facilitates remittance and reporting, ensuring the tax collected makes it to the tax authorities in full and on time. To encourage timely filing and remittance, many states allow retailers that file on time to keep a little of the sales tax they collect — typically between 0.5% and 5%, up to a maximum amount.

Wrapping Up

It’s clear that sales tax for online business can be incredibly complex, with rules and rates differing from state to state and product to product. With the right tax calculation tools on your business’s side, it’ll be easy to keep track of any tax obligations your business has accrued.

Leave a reply or comment below