Do you know which credit card pricing plan you’re on? This may seem like a basic question, but there’s a lot that goes into credit card payment processing. If you’re scratching your head, try thinking back to your initial merchant account setup.

If you were in a rush to get up and running (and who can blame you? The costs of starting even an online store are high), you may have partnered with a payment facilitator. These providers offer one pricing model — flat pricing. Just as the name indicates, this rate plan charges the same rate for every transaction you take. This rate is typically around 2.9% plus $0.10 - $0.30, so it can account for high-risk, high-reward cards. It attributes this high rate to every transaction because payment facilitators provide their merchants with one shared merchant account, so they can’t accommodate custom rate plans.

Now, if you instead remember waiting a few days, providing financial documents, undergoing a merchant account underwriting process and receiving an account approval, you may have a tiered or interchange-plus rate plan. Both of these rate plans are more cost-effective than flat-rate pricing, but for the purposes of this article we’ll focus on interchange-plus pricing.

What Is Interchange-Plus Pricing?

Interchange is the wholesale cost to run a given credit card transaction. Interchange is set by the card brands (Visa, MasterCard, Discover and Amex), is adjusted biannually every April and October, and increases for higher-risk, higher-reward cards. An example of a low-cost card is an in-person debit card payment. Conversely, a platinum hotel rewards card is an example of a card with a high interchange cost.

So, unlike flat-rate pricing, which charges a higher rate to accommodate all cards and payment methods, interchange-plus pricing charges the wholesale interchange cost plus a small provider markup.

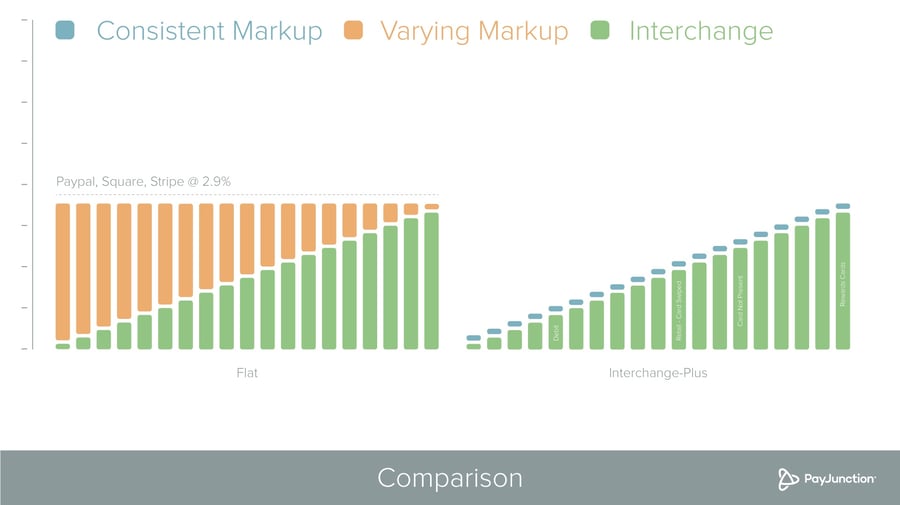

Here’s an illustration of these two plans side-by-side.

As you can see, interchange-plus pricing is a more cost-effective rate plan because merchants save money on low- to medium-cost transactions. It’s also a more transparent plan, as you know exactly how much money is going to your provider versus the card brands.

Is Interchange-Plus Right for Your Business?

Saving money is great, but before you think about switching rate plans, it’s important to know some of the nuances of interchange-plus pricing.

For one, this pricing plan is — again — not available with payment facilitators. So, if you’re looking to make the switch to save money on your rates, you may have to switch providers. This can get tricky if you’re in a contract with your current provider, although some businesses find that the cost savings compensate for their contract exit fees within months.

Next, because this plan is only available to merchants that are properly underwritten, you must have enough financial history and good financial standing to qualify for a merchant account. Why? Because a merchant account is essentially a loan. If your business is hit with a large chargeback that it cannot pay, your merchant service provider will cover the cost. Therefore, your provider needs to be able to assess your risk.

To establish credibility, you must be able to produce financial documents, which often include two recent months of merchant statements (if you’re already processing credit card payments), your business’s lease or deed, information regarding previous account terminations or bankruptcy, and bank account balances.

While this process may just sound like red tape, it’s important to note that proper merchant underwriting can prevent inconveniences like held funds, which is when your deposits are withheld because your provider anticipates an upcoming chargeback or potential fraud. Held funds often occur on high-ticket-value purchases. If your funds are held, you can’t touch that money, even though it’s rightfully yours. This situation does not occur with merchant service providers that underwrite your merchant account.

Lastly, your merchant statement will be more complex to review if you’re on interchange-plus pricing due to the different rates charged for each card. There are literally dozens of different rates that can be attributed to your transactions with this model, which makes it easier for unsavory providers to do things like pad your interchange rates. Spotting these fraudulent fees can be challenging because it takes a trained eye to know the correct interchange rates offhand. No matter what your rate plan is, we recommend always partnering with forthright merchant service providers.

If you’re just getting started with your e-commerce or retail business, flat-rate pricing can be a fast solution that’s easy to qualify for. However, over time as you gain loyal customers and increase your processing volume, you’ll want to look for more cost-effective ways to accept credit card payments. Your rate plan is the best place to start.

Leave a reply or comment below